Effective Debt Management Strategies

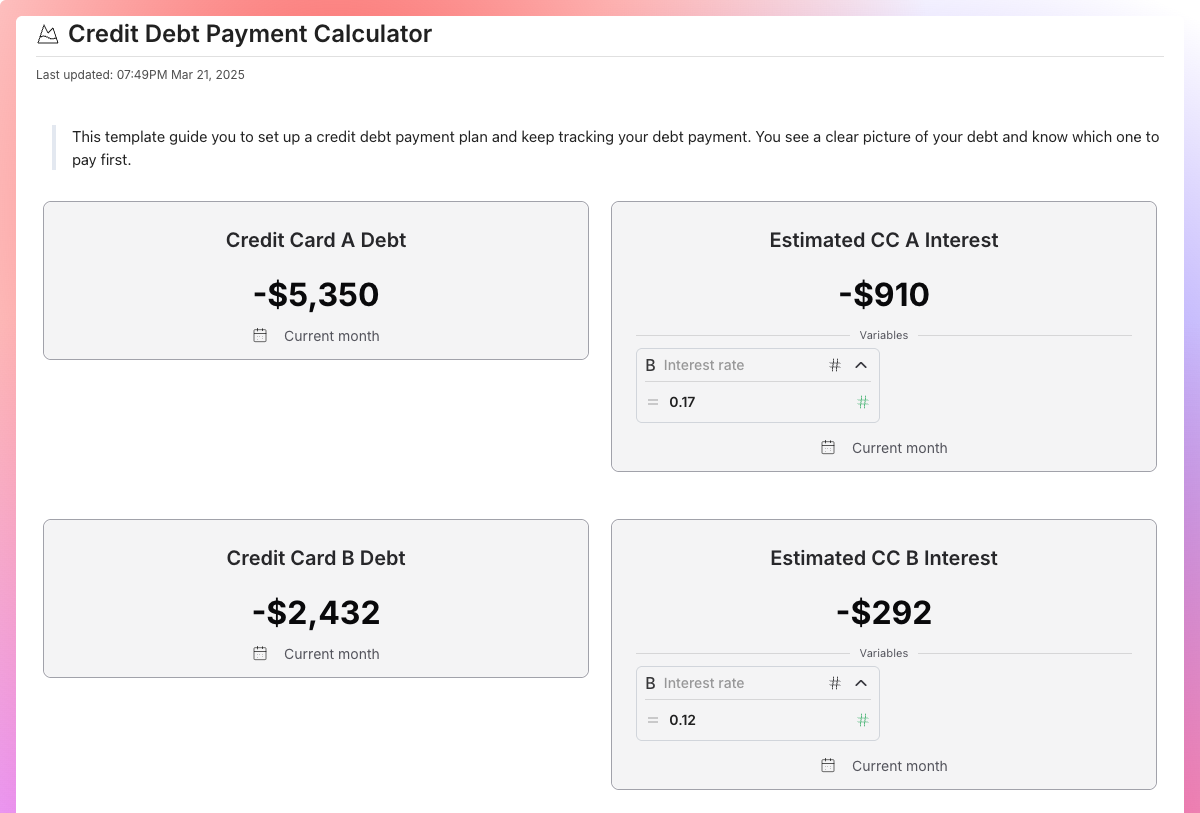

Debt Template: https://app.fina.money/t/3PONM4DGjUY90T?snap=1

Debt Template: https://app.fina.money/t/3PONM4DGjUY90T?snap=1

Intro

In today's fast-paced world, debt has become a common yet complex challenge in personal finance. From credit cards to student loans, mortgages to personal loans, debt can be overwhelming, often casting a long shadow over financial freedom and peace of mind. However, it's crucial to understand that debt doesn't have to be a perpetual burden. With the right strategies, managing and eventually paying off your debt is not just a possibility, but an achievable goal.

This article delves into the various proven strategies for debt management, offering practical steps and advice to guide you out of debt. Whether you're grappling with a small balance on your credit card or facing more substantial debts, the journey to a debt-free life begins with understanding and strategy. So, let's embark on this journey together, exploring how you can regain control of your finances and pave the way for a more secure and prosperous future.

Understanding Your Debt

Know What You Owe

The first step in effective debt management is clearly knowing your total debt and understanding debt consolidation options. It's not just about knowing how much you owe, but also understanding the finer details – the types of debt you have, their respective interest rates, the minimum monthly payments, and their due dates. This clarity is crucial in formulating a plan that's not only effective but also tailored to your unique financial situation.

Creating a Debt Inventory

A practical way to keep track of your debts is by creating a comprehensive list inside of Fina or a spreadsheet. This inventory should include:

-

The Name of the Creditor: Knowing who you owe and having their contact information can be helpful, especially if you need to negotiate terms later.

-

The Total Amount Owed: List the total outstanding balance for each debt.

-

Interest Rates: Document the interest rate for each debt, as this will influence which debt you might want to pay off first.

-

Monthly Payment: Note down the minimum monthly payment required for each debt.

-

Due Date: Keeping track of when each payment is due helps avoid late fees and additional interest charges.

This inventory not only provides a clear picture of your debts but also helps in prioritizing them, a crucial step in effective debt management. By understanding the magnitude and nature of your debts, you can start to plan a strategic approach to tackle them, one step at a time.

Strategies for Paying Off Debt

- The Debt Snowball Method The debt snowball method is a strategy designed to help you build momentum as you tackle your debt. Here's how it works:

-

List Your Debts from Smallest to Largest: Regardless of interest rates, order your debts from the smallest amount owed to the largest.

-

Focus on the Smallest Debt: Pay the minimum on all your debts except for the smallest one. For this smallest debt, pay as much as you can afford.

-

Celebrate the Wins: Once the smallest debt is paid off, take the amount you were paying on that debt and apply it to the next smallest debt, in addition to its minimum payment. This 'snowball' effect allows you to pay off each subsequent debt more quickly.

-

Repeat the Process: Continue this process, rolling over payments from debts you’ve cleared to those still outstanding.

This method is particularly effective because of the psychological wins. Paying off smaller debts first can provide a sense of accomplishment and motivate you to keep going.

- The Debt Avalanche Method The debt avalanche method is an alternative approach that prioritizes debts with the highest interest rates.

Here’s how it is structured:

-

List Your Debts by Interest Rate: Start by listing your debts in order from the highest to the lowest interest rate.

-

Prioritize High-Interest Debts: Allocate as much money as possible to the debt with the highest interest rate, while paying the minimum on your other debts.

-

Maximize Interest Savings: As you pay off the highest-interest debt, move to the debt with the next highest interest rate. The money saved on interest accelerates the repayment of other debts.

-

Continue the Process: Keep repeating this method, always focusing on the debt with the highest interest rate until all debts are cleared.

The advantage of the debt avalanche method is its financial efficiency. By focusing on high-interest debts first, you minimize the total interest paid over time, making it a cost-effective strategy.

Both the snowball and avalanche methods have their benefits. The snowball method can be more motivating due to quick wins, while the avalanche method is more efficient in terms of interest savings. The key is to choose the method that aligns best with your financial situation and psychological needs. By sticking to your chosen method, you can systematically reduce your debt burden and eventually achieve a debt-free life.

Additional Strategies for Unique Debt Management Circumstances

Debt Consolidation

Debt consolidation is a strategy where you combine multiple debts into a single loan, typically with a lower interest rate. This can simplify your payments and potentially reduce the amount of interest you pay over time. Options for consolidation include personal loans, balance transfer credit cards, or home equity loans. However, it's essential to be cautious and ensure that the consolidation actually results in financial benefit and doesn’t extend your debt period unnecessarily.

Negotiating with Creditors Sometimes, negotiating directly with your creditors can lead to more favorable terms. You might be able to reduce your interest rates, get a payment holiday, or even settle for a lesser amount than what you owe. Be honest about your financial situation, and don’t hesitate to ask for help. Creditors are often willing to negotiate to ensure they get some repayment rather than risk getting nothing.

Budget Adjustment Revising your budget is crucial in managing debt. Look for ways to reduce your expenses and increase your income. Even small adjustments can free up more money for debt repayment. Consider cutting back on non-essential expenses, looking for ways to save on everyday expenditures, and exploring side jobs or freelance opportunities for additional income.

Use Windfalls Wisely Any unexpected cash inflows, like tax refunds, bonuses, or gifts, should be directed towards debt repayment. While it might be tempting to use this money for other purposes, applying it to your debt can significantly accelerate your journey to becoming debt-free.

Credit Counseling Services For those who feel overwhelmed by their debt situation, credit counseling services can offer valuable assistance. These non-profit agencies can help you develop a debt management plan, and they often have the ability to negotiate with creditors on your behalf. They can also provide financial education and budgeting advice to help prevent future debt problems.

Each of these strategies offers a different approach to tackling debt, and they can be used individually or in combination, depending on your specific circumstances. Remember, the path to becoming debt-free requires patience, discipline, and a commitment to making sometimes challenging financial decisions. By applying these strategies thoughtfully, you can work towards a future free of financial burdens.

Embracing a Debt-Free Life

Achieving a debt-free status is not just about paying off what you owe; it's about embracing a lifestyle that prevents falling back into the debt trap. Maintaining a debt-free life involves continuous budget management, wise spending decisions, and regular financial reviews. It's about creating a sustainable financial plan that aligns with your long-term goals and values.

As you journey towards and maintain a debt-free life, it's important to have the right tools and resources at your disposal. This is where Fina, our financial software, can be a game-changer. Fina offers a comprehensive suite of tools designed to help you manage your finances effectively. With features such as budget tracking, expense categorization, and financial goal setting, Fina empowers you to take control of your financial life.

Remember, managing debt and maintaining a debt-free life is a journey that requires commitment, discipline, and the right tools. As always, we’re here to help and we wish you the best of luck on overcoming any debt you may have incurred.

Go transform your financial future! 🙂